All Categories

Featured

Table of Contents

[/image][=video]

[/video]

When the main annuity owner passes away, a picked beneficiary remains to get either 50% or 100% of the revenue forever. 60 years 6,291.96 6.29% Requirement Life 65 years 6,960.24 6.96% Canada Life 70 years 7,776.60 7.78% Canada Life 75 years 8,941.56 8.94% Canada Life The present ideal 50% joint life annuity price for a 65-year-old male is 6.96% from Canada Life, which is 0.24% less than the most effective price in February.

refers to the person's age when the annuity is established. These tables show annuities where income settlements remain degree throughout of the annuity. Escalating strategies are additionally readily available, where repayments begin at a lower degree yet raise each year according to the Retail Rates Index or at a set price.

For both joint life instances, numbers revealed are based on the initial life being male, and the beneficiary being a lady of the same age. Single life, level 7,545.60 7,554.12 7,458.72 7,496.40 7,435.08 7,444.92 Single life, escalating at 3% 5,390.40 5,399.16 5,341.80 5,425.80 5,673.36 5,535.84 Single life, rising at RPI 4,795.92 4,804.80 4,722.96 4,778.28 5,067.96 4,946.16 Joint life 50% 6,952.92 6,960.96 6,834.12 6,896.76 7,143.84 7,064.64 Joint life 100% 6,385.68 6,392.64 6,262.92 6,318.60 6,683.76 6,691.80 Details on historical annuity prices from UK carriers, generated by Retired life Line's in-house annuity quote system (commonly at or near the very first day of every month).

Additionally: is where payments start at a lower level than a degree plan, but boost at 3% yearly. is where settlements start at a reduced degree than a level strategy, yet increase each year in line with the Retail Rate Index. Use our interactive slider to show how annuity rates and pension plan pot dimension influence the earnings you could get: Annuity prices are an essential element in identifying the level of income you will certainly receive when buying an annuity with your pension plan financial savings.

The greater annuity rate you protect, the even more income you will obtain. If you were buying a life time annuity with a pension fund of 100,000 and were supplied an annuity rate of 5%, the annual income you get would be 5,000. Annuity prices vary from carrier to provider, and service providers will use you a customised price based on a variety of aspects including underlying economic aspects, your age, and your wellness and lifestyle for lifetime annuities.

This gives you certainty and reassurance regarding your long-term retired life revenue. Nevertheless, you might have an escalating life time annuity. This is where you can select to start your settlements at a lower level, and they will certainly after that raise at a fixed percent or according to the Retail Cost Index.

Annuities Hargreaves Lansdown

With both of these options, as soon as your annuity is set up, it can not typically be transformed., the rate remains the very same up until the end of the picked term.

It may amaze you to discover that annuity prices can differ significantly from provider-to-provider. At Retired life Line we have actually discovered a distinction of as much as 15% between the cheapest and greatest rates available on the annuity market. Retirement Line specialises in supplying you a contrast of the most effective annuity prices from leading carriers.

Annuity suppliers normally purchase federal government bonds (also recognized as gilts) to money their customers' annuities. The government pays a type of rate of interest referred to as the gilt yield to the annuity service provider. This in turn funds the routine income settlements they make to their annuity customers. Providers fund their annuities with these bonds/gilts due to the fact that they are among the most safe types of financial investment.

When the Financial institution Rate is reduced, gilt returns are also low, and this is shown in the pension plan annuity rate. On the various other hand, when the Financial institution Rate is high, gilt yields and regular annuity prices likewise have a tendency to climb.

Annuity carriers use added economic and industrial variables to determine their annuity rates. This is why annuity prices can rise or drop no matter what occurs to the Bank Price or gilt returns. The vital thing to keep in mind is that annuity prices can change often. They additionally commonly differ from provider-to-provider.

Security Benefit Annuity Reviews

This was of training course great news to individuals who were ready to transform their pension pot right into a guaranteed revenue. Canada Life's record at that time mentioned a benchmark annuity for a 65-year-old using 100,000 to purchase an annuity paying a yearly life time earnings of 6,873 per year.

This is since companies won't simply base your rate on your age and pension fund dimension. They will instead base it on your specific personal circumstances and the kind of annuity you want to take. This details is for illustrative purposes only. As we have defined above, your annuity provider will certainly base their annuity rate on economic and commercial elements, including present UK gilt yields.

Pba Annuity Fund

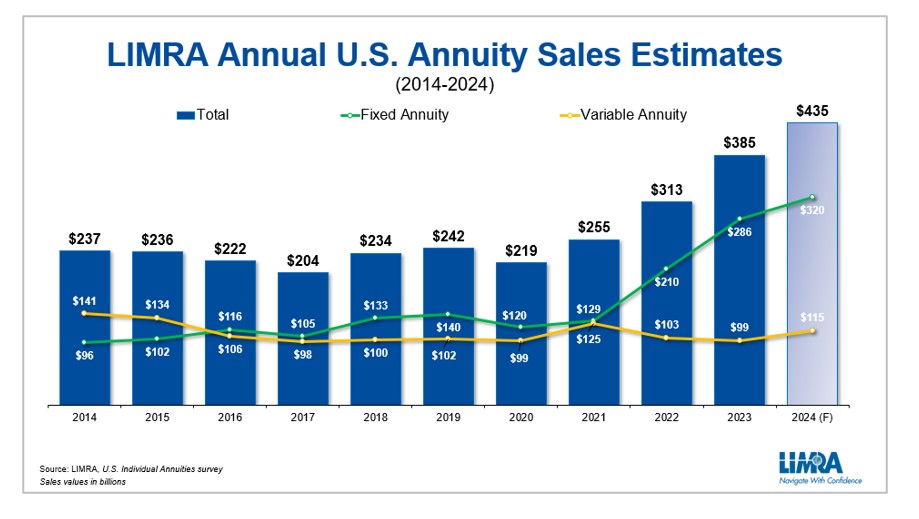

In 2025, LIMRA is forecasting FIA sales to go down 5%-10% from the document set in 2024 however remain over $100 billion. RILA sales will certainly note its 11th successive year of record-high sales in 2024.

LIMRA is forecasting 2025 VA sales to be level with 2024 results. After record-high sales in 2023, income annuities moved by compelling demographics trends and attractive payment prices need to exceed $18 billion in 2024, establishing another record. In 2025, lower rates of interest will certainly urge carriers to drop their payout prices, causing a 10% cut for revenue annuity sales.

Venerable Insurance And Annuity

It will certainly be a mixed expectation in 2025 for the overall annuity market. While market problems and demographics are extremely desirable for the annuity market, a decline in rate of interest rates (which thrust the impressive growth in 2023 and 2024) will certainly undercut fixed annuity products continued development. For 2024, we anticipate sales to be even more than $430 billion, up in between 10% to 15% over 2023.

The firm is also a struck with representatives and customers alike. "They're A+ rated.

The business sits atop one of the most current version of the J.D. Power Overall Client Contentment Index and flaunts a solid NAIC Issue Index Rating, too. Pros Industry leader in customer fulfillment Stronger MYGA rates than a few other very rated companies Cons Online item info could be more powerful Much more Insights and Experts' Takes: "I have never had a poor experience with them, and I do have a number of happy customers with them," Pangakis claimed of F&G.

The company's Secure MYGA includes benefits such as riders for terminal illness and retirement home arrest, the ability to pay the account worth as a survivor benefit and rates that go beyond 5%. Few annuity business excel greater than MassMutual for consumers who value financial stamina. The company, established in 1851, holds a prominent A++ score from AM Best, making it among the most safe and best business readily available.

"I have actually heard a whole lot of advantages concerning them." MassMutual markets numerous solid items, consisting of earnings, repaired and variable options. Its Steady Voyage annuity, for instance, supplies a traditional way to generate income in retired life paired with convenient abandonment fees and various payment alternatives. The firm additionally markets licensed index-linked annuities through its MassMutual Ascend subsidiary.

Athene Annuity & Life Assurance Company Subsidiaries

"Nationwide stands out," Aamir Chalisa, general supervisor at Futurity First Insurance policy Team, told Annuity.org. "They've obtained impressive customer support, a very high ranking and have been around for a number of years. We see a great deal of clients requesting for that." Annuities can provide considerable worth to possible clients. Whether you want to generate revenue in retirement, grow your money without a great deal of danger or take advantage of high rates, an annuity can properly achieve your goals.

Annuity.org laid out to recognize the leading annuity companies in the sector. To achieve this, we created, tested and implemented a fact-based methodology based on crucial industry aspects. These consist of a company's financial toughness, accessibility and standing with clients. We likewise contacted several sector experts to get their takes on different business.

{kind=link}

Latest Posts

Index Annuity With Income Rider

How Are Inherited Annuities Taxed

Best Fixed Index Annuity With Income Rider