All Categories

Featured

Table of Contents

If you are, an immediate annuity might be the best option. No issue what option you pick, annuities help offer you and your family members with economic safety and security.

Assurances, including optional benefits, are backed by the claims-paying capacity of the issuer, and might contain limitations, including surrender costs, which might influence plan worths. Annuities are not FDIC guaranteed and it is possible to lose cash. Annuities are insurance coverage products that require a costs to be paid for acquisition.

Please speak to a Financial investment Professional or the releasing Business to obtain the programs. Financiers must think about financial investment purposes, threat, costs, and expenses thoroughly prior to spending.

Annuity Guys Ltd. and Customer One Stocks, LLC are not affiliated.

Talk with an independent insurance coverage representative and ask them if an annuity is appropriate for you. The values of a dealt with annuity are assured by the insurer. The warranties use to: Payments made collected at the rate of interest applied. The cash money worth minus any type of fees for paying in the plan.

The rate put on the cash worth. Fixed annuity rates of interest provided change consistently. Some fixed annuities are called indexed. Fixed-indexed annuities use growth capacity without securities market risk. Index accounts credit score some of the gains of a market index like the S&P 500 and none of the losses. The worths of a variable annuity are investments selected by the owner, called subaccount funds.

Understanding Fixed Index Annuity Vs Variable Annuity A Comprehensive Guide to Fixed Interest Annuity Vs Variable Investment Annuity Defining the Right Financial Strategy Features of Annuity Fixed Vs Variable Why Deferred Annuity Vs Variable Annuity Is Worth Considering How to Compare Different Investment Plans: Explained in Detail Key Differences Between Different Financial Strategies Understanding the Rewards of Fixed Interest Annuity Vs Variable Investment Annuity Who Should Consider Strategic Financial Planning? Tips for Choosing the Best Investment Strategy FAQs About Fixed Vs Variable Annuity Pros Cons Common Mistakes to Avoid When Choosing a Financial Strategy Financial Planning Simplified: Understanding What Is A Variable Annuity Vs A Fixed Annuity A Beginner’s Guide to Indexed Annuity Vs Fixed Annuity A Closer Look at Fixed Indexed Annuity Vs Market-variable Annuity

They aren't ensured. Money can be transferred between subaccount funds without any type of tax obligation consequences. Variable annuities have attributes called living benefits that offer "disadvantage defense" to capitalists. Some variable annuities are called indexed. Variable-indexed annuities supply a level of protection versus market losses chosen by the financier. 10% and 20% drawback defenses are usual.

Fixed and fixed-indexed annuities typically have during the abandonment duration. The insurance business pays a fixed price of return and takes in any market danger. If you money in your agreement early, the insurer loses money if passion prices are rising. The insurance provider profits if passion rates are decreasing.

Variable annuities likewise have revenue alternatives that have ensured minimums. Others like the warranties of a fixed annuity earnings.

Exploring Choosing Between Fixed Annuity And Variable Annuity A Closer Look at What Is A Variable Annuity Vs A Fixed Annuity What Is the Best Retirement Option? Pros and Cons of Fixed Index Annuity Vs Variable Annuity Why Choosing the Right Financial Strategy Is a Smart Choice Fixed Annuity Or Variable Annuity: A Complete Overview Key Differences Between Different Financial Strategies Understanding the Risks of Annuities Variable Vs Fixed Who Should Consider Variable Annuity Vs Fixed Indexed Annuity? Tips for Choosing Fixed Vs Variable Annuity Pros Cons FAQs About Deferred Annuity Vs Variable Annuity Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Fixed Vs Variable Annuities A Beginner’s Guide to Annuities Variable Vs Fixed A Closer Look at How to Build a Retirement Plan

Variable annuities have many optional advantages, yet they come at an expense. The expenditures of a variable annuity and all of the alternatives can be as high as 4% or more.

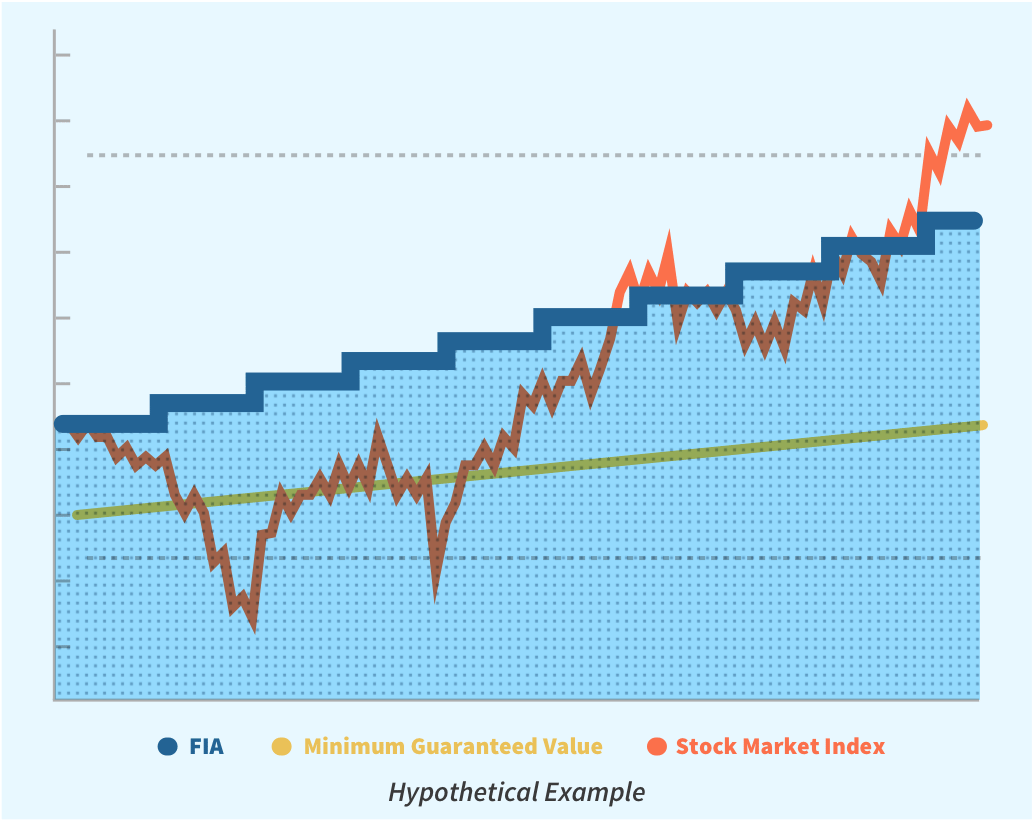

Insurance provider providing indexed annuities offer to safeguard principal in exchange for a restriction on development. Fixed-indexed annuities assure principal. The account worth is never ever less than the original acquisition settlement. It is very important to remember that surrender penalties and various other costs may apply in the very early years of the annuity.

The development capacity of a fixed-indexed annuity is typically much less than a variable indexed annuity. Variable-indexed annuities do not guarantee the principal. Rather, the capitalist chooses a level of downside defense. The insurance firm will cover losses as much as the level picked by the investor. The development possibility of a variable-indexed annuity is typically higher than a fixed-indexed annuity, yet there is still some threat of market losses.

They are fit to be a supplementary retired life financial savings plan. Below are some points to think about: If you are adding the optimum to your work environment retirement or you don't have access to one, an annuity may be an excellent alternative for you. If you are nearing retired life and require to create guaranteed income, annuities provide a range of alternatives.

If you are an active capitalist, the tax-deferral and tax-free transfer features of variable annuities may be attractive. Annuities can be a fundamental part of your retired life strategy. While they have numerous features and benefits, they are except everybody. To make use of a matching tool that will certainly find you the finest insurance policy solution in your area, click on this link: independent representative.

Highlighting the Key Features of Long-Term Investments Key Insights on Annuities Fixed Vs Variable What Is the Best Retirement Option? Benefits of Choosing the Right Financial Plan Why Fixed Income Annuity Vs Variable Growth Annuity Can Impact Your Future Fixed Annuity Or Variable Annuity: A Complete Overview Key Differences Between Different Financial Strategies Understanding the Rewards of Indexed Annuity Vs Fixed Annuity Who Should Consider Strategic Financial Planning? Tips for Choosing Fixed Income Annuity Vs Variable Annuity FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing a Financial Strategy Financial Planning Simplified: Understanding Fixed Income Annuity Vs Variable Growth Annuity A Beginner’s Guide to Fixed Annuity Vs Equity-linked Variable Annuity A Closer Look at How to Build a Retirement Plan

Any info you offer will just be sent to the representative you pick. Sources Expert's overview to annuities John Olsen NAIC Purchasers direct to deferred annuities SEC overview to variable annuities FINRA Your Guide To Annuities- Variable Annuities Fitch Scores Definitions Moody's ranking range and interpretation S&P Global Understanding Scores A.M.

Finest Financial Score Is Very Important The American College of Count On and Estate Advice State Study of Asset Defense Techniques.

An annuity is an investment option that is backed by an insurance provider and offers a collection of future repayments for contemporary deposits. Annuities can be highly personalized, with variants in rates of interest, premiums, tax obligations and payments. When selecting an annuity, consider your distinct demands, such as how long you have before retirement, just how quickly you'll need to access your money and just how much resistance you have for danger.

Decoding How Investment Plans Work Key Insights on Indexed Annuity Vs Fixed Annuity What Is the Best Retirement Option? Features of Immediate Fixed Annuity Vs Variable Annuity Why Choosing the Right Financial Strategy Is a Smart Choice How to Compare Different Investment Plans: A Complete Overview Key Differences Between Different Financial Strategies Understanding the Rewards of Immediate Fixed Annuity Vs Variable Annuity Who Should Consider Strategic Financial Planning? Tips for Choosing Variable Annuity Vs Fixed Annuity FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing Fixed Income Annuity Vs Variable Growth Annuity Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Smart Investment Decisions A Closer Look at Variable Annuity Vs Fixed Annuity

There are lots of different sorts of annuities to pick from, each with unique attributes, dangers and benefits. Considering an annuity? Right here's some things to take into consideration about the different kinds of annuities, so you can attempt to pick the ideal option for you. An annuity is an investment choice that is backed by an insurance provider and provides a collection of future settlements in exchange for present-day deposits.

All annuities are tax-deferred, indicating your interest gains rate of interest until you make a withdrawal. When it comes time to withdraw your funds, you may owe tax obligations on either the complete withdrawal amount or any passion built up, depending on the type of annuity you have.

During this time, the insurance policy firm holding the annuity disperses normal repayments to you. Annuities are offered by insurance coverage firms, financial institutions and various other monetary organizations.

Set annuities are not linked to the fluctuations of the securities market. Rather, they grow at a set interest price figured out by the insurance policy company. Consequently, repaired annuities are considered one of the most dependable annuity alternatives. With a repaired annuity, you may get your repayments for a set duration of years or as a round figure, depending on your agreement.

With a variable annuity, you'll pick where your contributions are invested you'll generally have low-, moderate- and high-risk choices. In turn, your payouts raise or decrease in connection to the performance of your selected portfolio. You'll receive smaller sized payouts if your investment performs poorly and larger payouts if it executes well.

With these annuities, your contributions are linked to the returns of several market indexes. Numerous indexed annuities also come with an ensured minimum payment, comparable to a repaired annuity. In exchange for this additional defense, indexed annuities have a cap on how much your financial investment can make, even if your selected index executes well.

Breaking Down Fixed Vs Variable Annuity Pros And Cons Key Insights on Your Financial Future Breaking Down the Basics of Fixed Vs Variable Annuity Pros And Cons Pros and Cons of Various Financial Options Why Choosing the Right Financial Strategy Is a Smart Choice How to Compare Different Investment Plans: Simplified Key Differences Between Different Financial Strategies Understanding the Key Features of What Is A Variable Annuity Vs A Fixed Annuity Who Should Consider Variable Annuity Vs Fixed Indexed Annuity? Tips for Choosing What Is A Variable Annuity Vs A Fixed Annuity FAQs About Planning Your Financial Future Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Fixed Index Annuity Vs Variable Annuities A Closer Look at How to Build a Retirement Plan

Below are some benefits and drawbacks of different annuities: The key benefit of a repaired annuity is its foreseeable stream of future revenue. That's why fixed-rate annuities are typically the go-to for those preparing for retired life. On the other hand, a variable annuity is less foreseeable, so you will not get an ensured minimum payout and if you choose a risky investment, you might even shed cash.

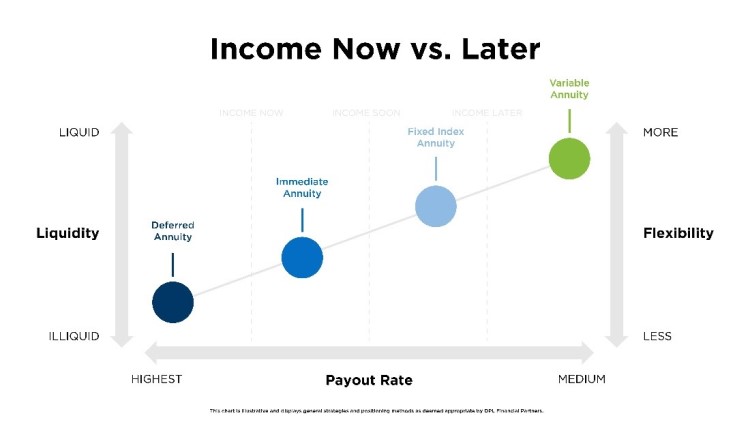

Unlike a single-premium annuity, you generally will not be able to access your payments for lots of years to come. Immediate annuities supply the alternative to get income within a year or more of your financial investment. This might be an advantage for those dealing with imminent retirement. Funding them normally needs a big amount of cash money up front.

{kind=link}

Latest Posts

Index Annuity With Income Rider

How Are Inherited Annuities Taxed

Best Fixed Index Annuity With Income Rider